ABSTRACT

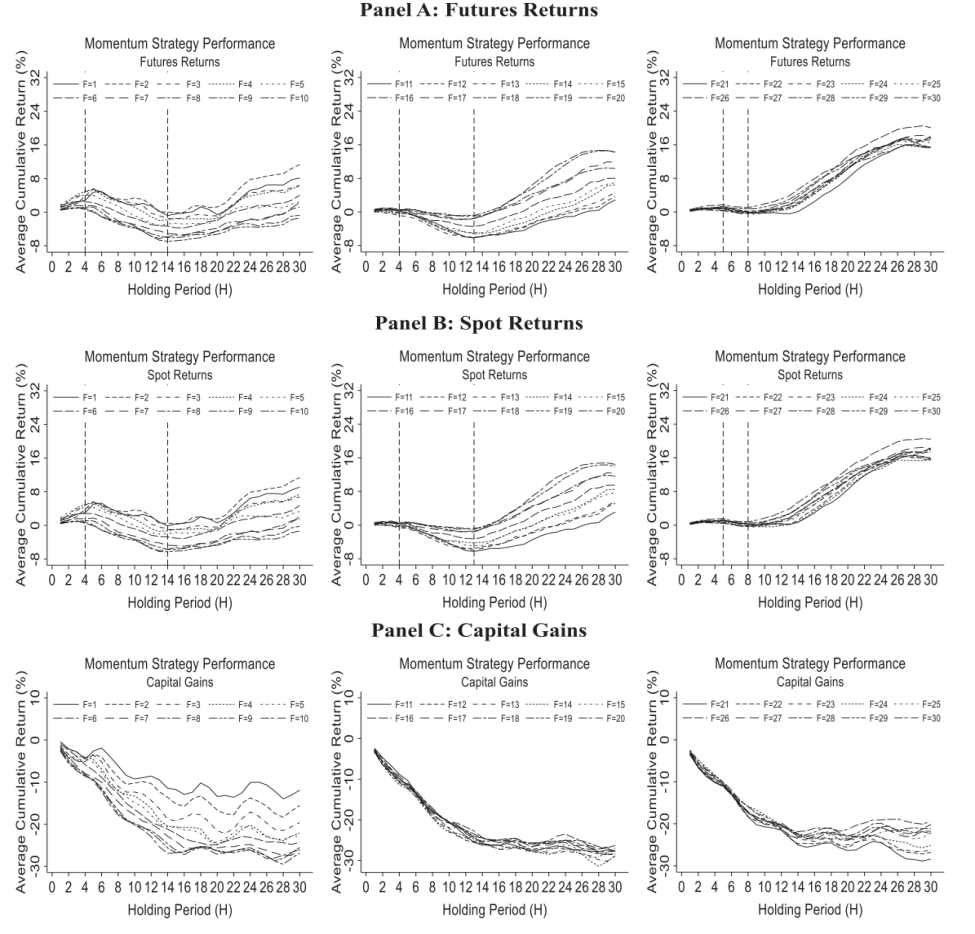

Questions as to why differences in momentum and reversal patterns seem to emerge in commodity futures compared with spot markets, and how these patterns can be explained, remain unanswered. To investigate these questions, I examine 23 commodities over a period of 60 years. I first show that including the net convenience yield in the definition of commodity spot returns reconciles the differences in the results for commodity spot and futures markets. Both commodity futures and spot markets exhibit quantitatively consistent momentum and reversal effects. An initial momentum effect is followed by a reversal effect and then another momentum effect. These observed patterns in commodities can be jointly explained by a combination of traditional asset pricing factors and a basis factor related to the net convenience yield.

KEYWORDS

asset pricing factors, commodity markets, convenience yield, momentum, reversal

JCR CLASSIFICATION

Q3

JEL CLASSIFICATION

G10, G11, G13, G14

Journal of Futures Markets

http://doi.org/10.1002/fut.22424