近日,北京师范大学湾区国际商学院助理教授王禹衡博士以第一作者身份在会计学领域重要期刊《Accounting, Auditing & Accountability Journal》上发表了题为《Contextualised accountant stereotypes: understanding their social construction and reconstruction in Chinese society》的研究论文,该期刊为全球排名前三的交叉学科会计期刊。

本文旨在了解会计刻板印象在中国社会的宏观、国家和结构层面是如何建构和重构的。作者通过采用贝克尔(1963)的标签理论对中国会计刻板印象的社会建构进行定性研究,将刻板印象视为一种社会建构的实践。利用后实证主义的反思性认识论,对会计师和相关行为者进行了28次半结构化访谈,并主题分析其内容。

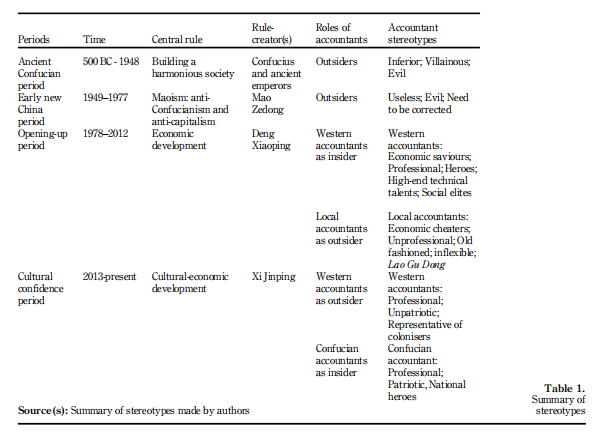

作者发现中国会计刻板印象是根据不同文化政治时期所创造和执行的规则来构建和重构的。古代儒家时期(公元前500年- 1948年)形成的会计刻板印象在1949年和2012年被取代,此时政治重点从封建主义转向宣传社会主义,又因转向发展经济而转变。它们还表明,2013年,儒家对会计的刻板印象重新出现,但被中央政府宣传儒家思想的文化自信政策所重构。从实证上看,先前的文献关注的是会计刻板印象是什么以及会计师如何应对这种刻板印象,但它忽略了这些会计刻板印象在政治和文化上的构建、扩散和合法化的方式。本文通过了解会计刻板印象在以前未被探索的政治文化背景下的社会实践,填补了这一空白。从理论上讲,通过在会计文献中首次使用贝克尔(1963)的标签理论,它进一步增强了我们对社会规则如何塑造会计师身份和社会地位的理解。

论文摘要:

Purpose – This study seeks to understand how accountant stereotypes have been constructed and reconstructed at the macro-national and the structural level in Chinese society.

Design/methodology/approach – This qualitative investigation into China’s social construction of accountant stereotypes employs Becker’s (1963) labelling theory. Viewing stereotyping as a socially constructed practice, this study draws on a post-positivistic, reflexive epistemology in conducting 28 semi- structured interviews with accountants and related actors.

Findings – Chinese accountant stereotypes are constructed and reconstructed according to the rules created and enforced in different cultural-political periods. The accountant stereotypes constructed during the ancient Confucian period (500 BC – 1948) were replaced during 1949 and 2012 when the political focus shifted towards propagating socialism and later promoting economic growth. They also show how Confucian stereotypes of accountants resurfaced in 2013 but were reconstructed by the central government’s cultural confidence policy of propagating Confucianism.

Originality/value – Empirically, prior literature has focused on what the accountant stereotype is and how accountants respond to such stereotypes, but it has neglected the ways in which these accountant stereotypes are politically and culturally constructed, diffused and legitimated. This paper fills in the gap by understanding the social practice of accountant stereotyping in a previously unexplored political-cultural context, namely Chinese society. In theoretical terms, by offering the first use of Becker’s (1963) labelling theory in the accounting literature, it furthermore enhances our understanding of how accountants’ identities and social standing are shaped by social rules.